We are in for a string of hotter than expected economic reports, starting with the jobs reports tomorrow morning. At least, that is what the bond market is suggesting if you are to take into account that the short end of the curve has gone vertical in recent weeks.

Of course, there are many who seem to attribute the recent rate surge to the markets getting their panties in a bunch over "seasonal blips" in recent economic reports. This type of dismissive optimism has kept the markets elevated, despite the fact that yields are commanding a much lower floor for equities presently.

With that said, the dismissive optimism of the past few weeks is about to turn into reluctant acceptance that there is a good chance we are now facing a second leg of inflationary pressures.

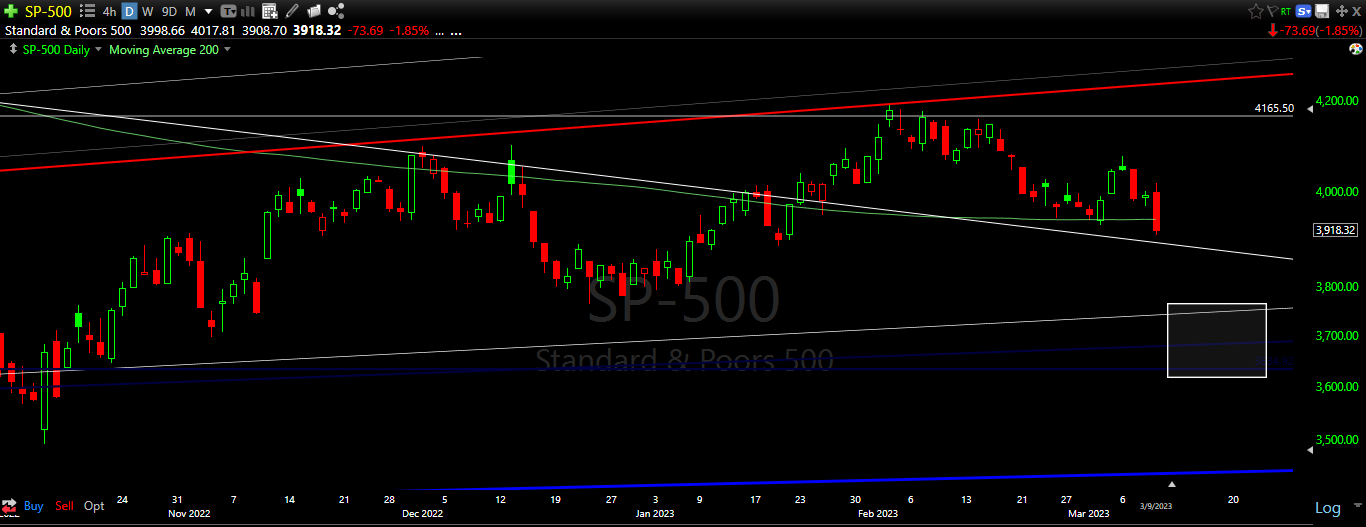

Tomorrow begins the trek down to the 3700 range, which is where the markets are likely to end up right as the March FOMC meeting kicks off a little less than two weeks from today.

There is a confluence of support beginning at SPX 3750 down to 3630. All of these support levels will be hit in the weeks ahead. It will be enough, however, for the SPX to move down to around the 3700-3750 mark by the 21st of March.

Expecting a hotter than expected NFP number tomorrow and I expect that today's volatility will only be expanded upon to the downside into the end of this week.

We remain short after adding to our short exposure on Tuesday.

Goodnight.

Zenolytics Turning Points is 300+ editions in and only getting better. Find out why institutions and individual investors have come to depend on our service through each and every type of market environment. Click here for details.

Disclaimer

This website is for informational purposes only and does not constitute a complete description of our investment advisory services. No information contained on this website constitutes investment advice.

This website should not be considered a solicitation, offer or recommendation for the purchase or sale of any securities or other financial products and services discussed herein. Viewers of this website will not be considered clients of T11 Capital Management LLC just by virtue of access to this website.

T11 Capital Management LLC only conducts business in jurisdictions where licensed, registered, or where an applicable registration exemption or exclusion exists. Information contained herein is not intended for persons in any jurisdiction where such distribution or use would be contrary to the laws or regulations of that jurisdiction, or which would subject T11 Capital Management LLC to any unintended registration requirements. Visitors to this site should not construe any discussion or information contained herein as personalized advice from T11 Capital Management LLC. Visitors should discuss the personal applicability of the specific products, services, strategies, or issues posted herein with a professional advisor of his or her choosing.

Information throughout this site, whether stock quotes, charts, articles, or any other statement or statements regarding capital markets or other financial information, is obtained from sources which we, and our suppliers believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. Neither our information providers nor we shall be liable for any errors or inaccuracies, regardless of cause, or the lack of timeliness of, or for any delay or interruption in, the transmission thereof to the user. With respect to information regarding financial performance, nothing on this website should be interpreted as a statement or implication that past results are an indication of future performance.