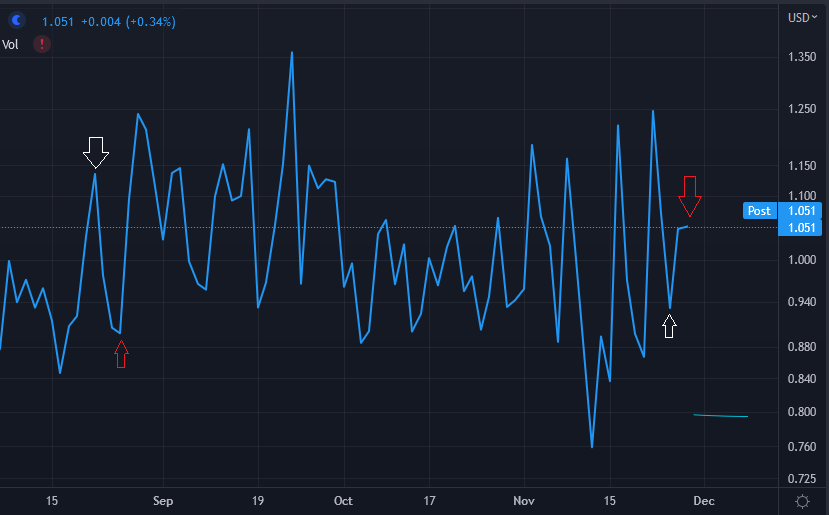

Put/call ratio first:

The white arrow shows where the put/call ratio started the week of the Powell speech for August vs. present.

Notice that going into the August speech, after a hunky dory post-FOMC conference in July, investors were actually looking forward to Powell giving them more ammunition on the upside. They were buying calls into the Jackson Hole speech without much hedging.

Today it's the polar opposite. We have an uptrending put/call into Powell's speech tomorrow, as investors are hedging the speech.

This type of pre-event hedging action typically leads to unwinds of those hedges once the event is finished, as the monster in the closet is a lot less scary once you open the door.

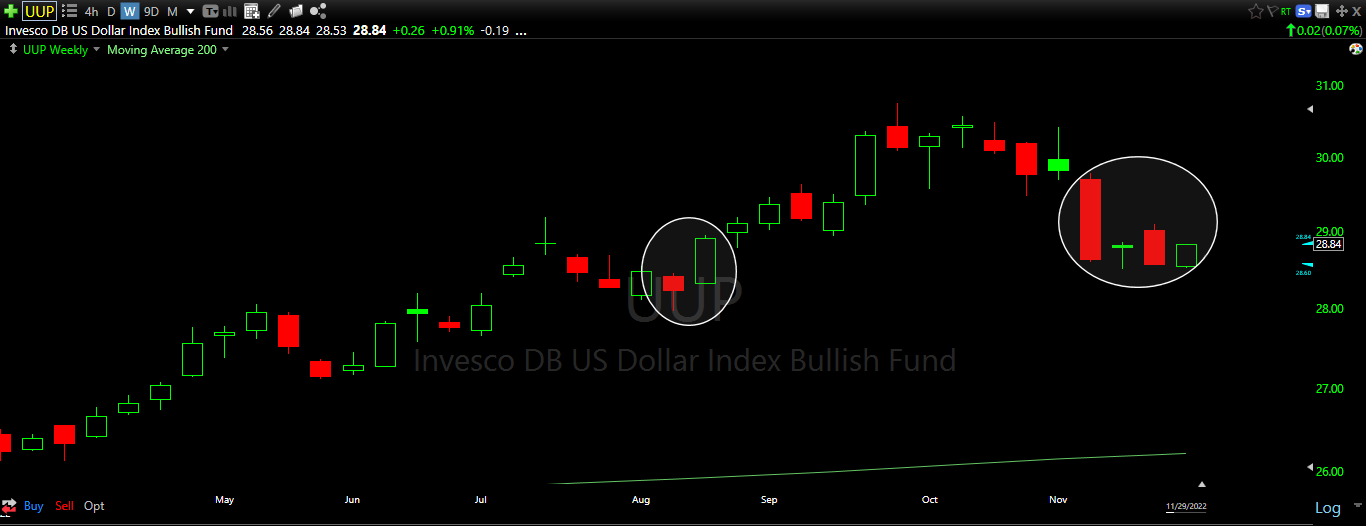

The next two charts demonstrate why irrespective of how Powell comes across tomorrow, he will have to acknowledge that the future path of tightening will be of less consequence than what they have done the past few meetings. In other words, no more 75 bp hikes. The upward velocity of rate hikes is finished.

Here is the USD:

Uptrending in August. Downtrending at present.

The foundation of the inflation argument has shifted. This means that there are very large amounts of capital restructuring their portfolios around a post-inflationary world. The restructuring of portfolios against such a massive macro trade as inflation has been over the past 12 months always begins with the largest market of all, which is the global currency market.

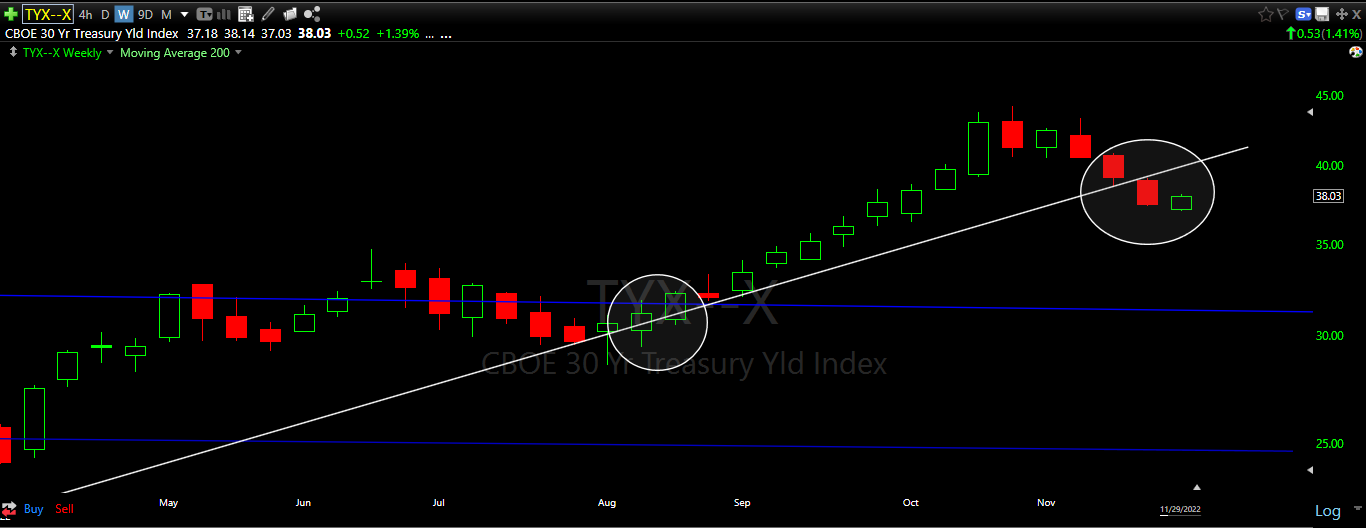

Third are interest rates:

Above trend with positive upside momentum in August. Below trend with positive downside momentum at present.

Rates have now shifted from betting on greater inflation to betting on a timeline for rate hikes to end.

All Powell has to say tomorrow is that the velocity of rate hikes is set to drop, confirming what both USD and rates are telling us.

That alone will set off an unwind of all the hedges that have been taken going into tomorrow's speech.

Remember, this isn't the market of August, June or March.

Back then none of us had any idea how far Powell would go, or how high the velocity of rate hikes would get. Now that we are on the back end of the rate hiking curve, he can be as hawkish as he wants tomorrow, but he will have to acknowledge that the velocity of hikes is set to drop....and that is all it will take.

Zenolytics Turning Points is 300+ editions in and only getting better. Find out why institutions and individual investors have come to depend on our service through each and every type of market environment. Click here for details

Disclaimer

This website is for informational purposes only and does not constitute a complete description of our investment advisory services. No information contained on this website constitutes investment advice.

This website should not be considered a solicitation, offer or recommendation for the purchase or sale of any securities or other financial products and services discussed herein. Viewers of this website will not be considered clients of T11 Capital Management LLC just by virtue of access to this website.

T11 Capital Management LLC only conducts business in jurisdictions where licensed, registered, or where an applicable registration exemption or exclusion exists. Information contained herein is not intended for persons in any jurisdiction where such distribution or use would be contrary to the laws or regulations of that jurisdiction, or which would subject T11 Capital Management LLC to any unintended registration requirements. Visitors to this site should not construe any discussion or information contained herein as personalized advice from T11 Capital Management LLC. Visitors should discuss the personal applicability of the specific products, services, strategies, or issues posted herein with a professional advisor of his or her choosing.

Information throughout this site, whether stock quotes, charts, articles, or any other statement or statements regarding capital markets or other financial information, is obtained from sources which we, and our suppliers believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. Neither our information providers nor we shall be liable for any errors or inaccuracies, regardless of cause, or the lack of timeliness of, or for any delay or interruption in, the transmission thereof to the user. With respect to information regarding financial performance, nothing on this website should be interpreted as a statement or implication that past results are an indication of future performance.