Every day I go through roughly 200 stocks/indices/indicators, several times per day, looking for signals, attempting to connect dots and ultimately, hoping to find risk/reward situations that create outperformance.

The title Lies, Damn Lies seems appropriate as when the markets want to reveal any kind of truth, they first do so through blatant lies. Conversely, whenever truth appears apparent, there is likely to be deception involved.

These are simply thoughts (some completely random) as I attempt to connect the dots:

- Insider buying is now at an 8 year high according to Bloomberg. "The last time insider buying spiked in this fashion, in August 2011, the S&P 500 was in the middle of a 19 percent retreat before staging a 10 percent rally in each of the next two quarters." Insiders are very obviously witnessing the fact that on a corporate level everything is fine. The weakness in the markets hasn't trickled down into the economy as of yet. Whether in two quarters from now those very same insiders are wishing they had put their cash in a bank CD due to a falling stock price and sudden economic weakness is another question entirely. Insiders are just as likely to blow it as anybody else, keep that in mind. For the time being, however, this is another indication that corporate earnings will calm the markets a bit in Q1.

- Short interest in various industry ETFs is plunging, which is basically the equivalent of soldiers putting down their guns in the middle of an oncoming assault. Either the soldiers have lost their minds or they don't think the assault is worth fighting against. The XLB (materials sector etf) is at a 4 month low in short interest. XLK (technology sector etf) is close to a three low in short interest. XLP (consumer staples) is sitting at a multi-year low in short interest, as well. From a purely contrarian perspective, this is a problem.

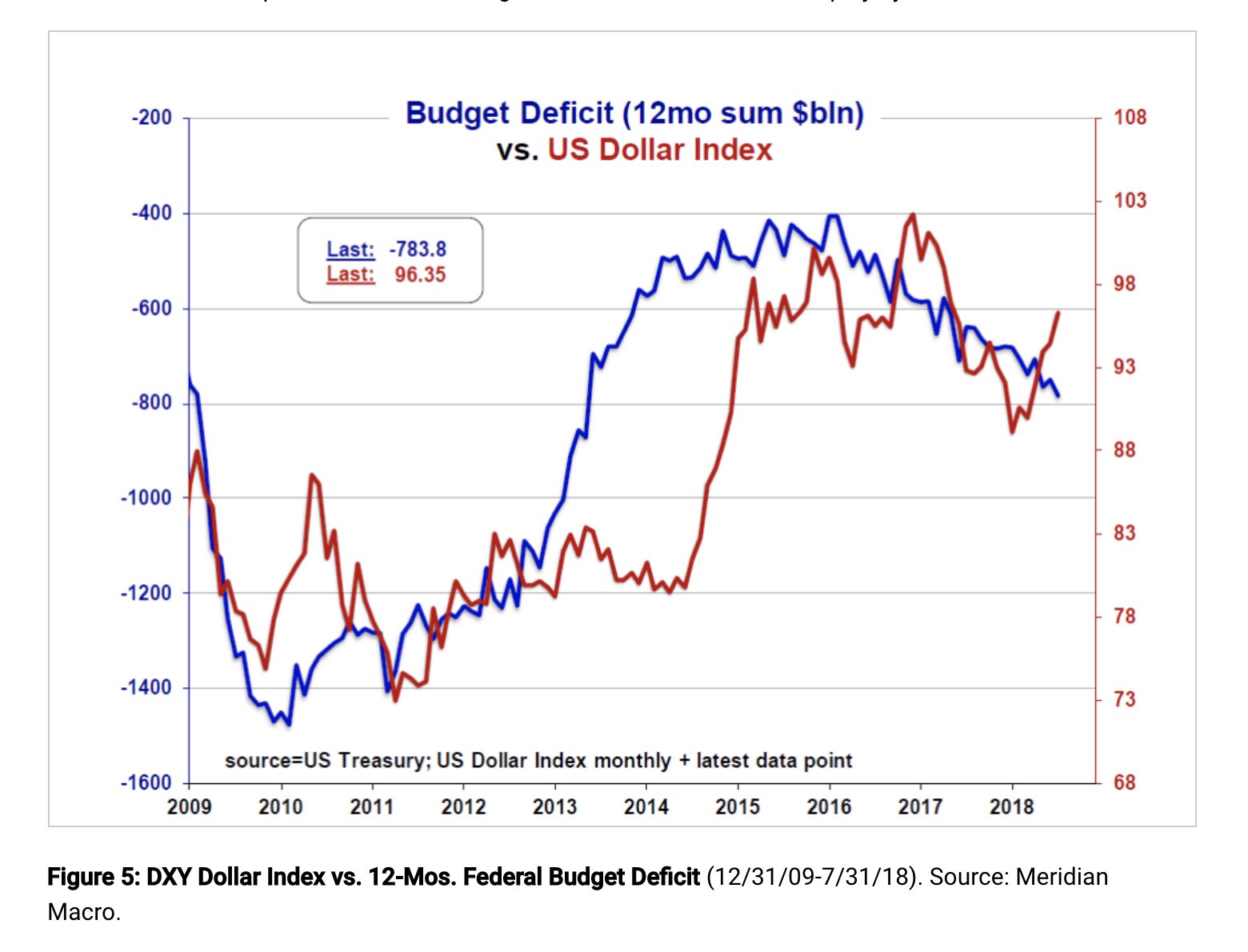

- Among developed countries, the United States is certainly an outlier when it comes to debt. This fact puts the Federal Reserve in a precarious position should another economic crisis take hold. In any case, the U.S. Dollar will be the most apparent casualty.

- The Fed expanding their balance sheet had a stupendous effect on equity prices. How can we logically assume then that through extensive global central bank balance sheet tightening, this effect won't reverse to an extent? We have already seen that in 2018 as the Fed's expanded tightening starting in October of $50 billion per month was accompanied by a market top. Europe climbs onboard the QT train in 2019. While the markets could very well rally in Q1, expect the entire structure of market rallies to change. The ultimate destination of future market rallies will be a selling opportunity as opposed to any semblance of the "buy the dip" mentality of the past few years.

- Investors have gold wrong here. The popular wisdom is that gold is rallying because investors are simply looking for a safe haven while pandemonium has broken loose in Wall Street Square Garden. What if gold is being bid here because of numerous macro-economic factors that ultimately have to do with the Fed backing themselves into a very tight corner that results in a much weaker dollar over the long-term?

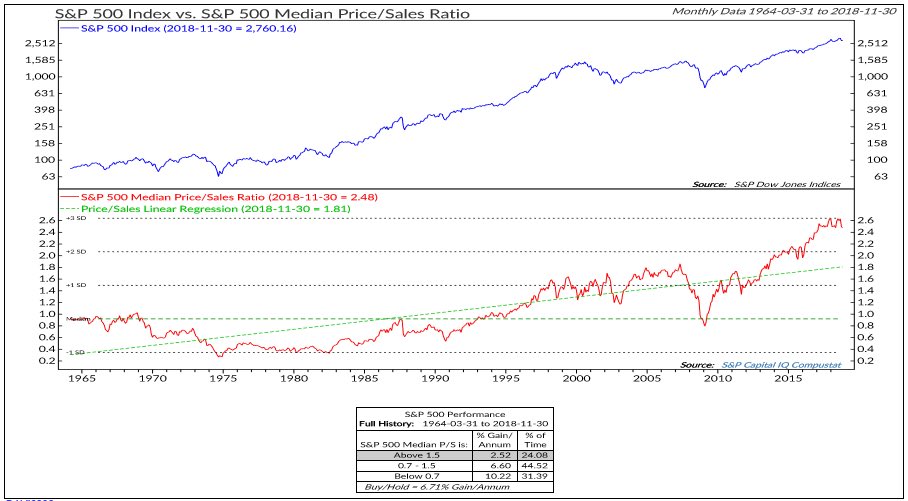

- There is some mean reversion in our future when it comes to price to sales ratios for the market. Doesn't play well into a slowing economic environment in 2019.

- Deficits drive the value of the U.S. Dollar

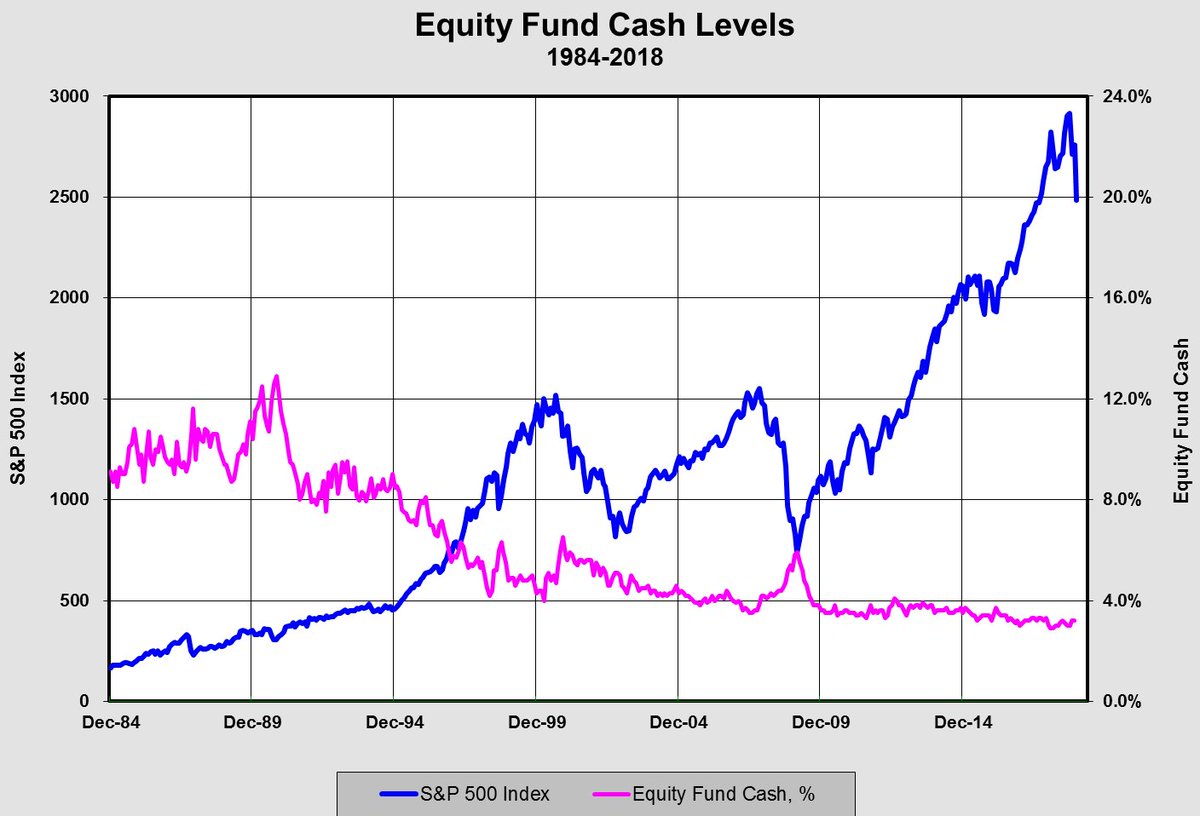

- Equity mutual fund cash levels will be subject to mean reversion throughout 2019 and 2020

- The thrust of last week's reversals to the upside in the major averages is worth noting. It's something we haven't seen in the markets for what seems like a millennia. When these types of moves take place during a period when nobody, including myself, was expecting them, it's worth paying attention. The market is attempting to zoom out of the train station with the least amount of passengers onboard.

- C and BRK.B look like some very plain vanilla ways to play a rebound in financials. Relatively low risk entry points here for a short to intermediate term bounce.

- MSFT has exhibited some very real relative strength. In all likelihood, January should be a much different month for the name than December.

- NFLX is the way to play "bullish on FANGs" down here.

_______________________________________________________________________________

From time to time, I email individual company research, commentary and excerpts from my monthly investor letter to those who are interested. If you would like to receive future emails, please write me at mail@T11Capital.com

Disclaimer

This website is for informational purposes only and does not constitute a complete description of our investment advisory services. No information contained on this website constitutes investment advice.

This website should not be considered a solicitation, offer or recommendation for the purchase or sale of any securities or other financial products and services discussed herein. Viewers of this website will not be considered clients of T11 Capital Management LLC just by virtue of access to this website.

T11 Capital Management LLC only conducts business in jurisdictions where licensed, registered, or where an applicable registration exemption or exclusion exists. Information contained herein is not intended for persons in any jurisdiction where such distribution or use would be contrary to the laws or regulations of that jurisdiction, or which would subject T11 Capital Management LLC to any unintended registration requirements. Visitors to this site should not construe any discussion or information contained herein as personalized advice from T11 Capital Management LLC. Visitors should discuss the personal applicability of the specific products, services, strategies, or issues posted herein with a professional advisor of his or her choosing.

Information throughout this site, whether stock quotes, charts, articles, or any other statement or statements regarding capital markets or other financial information, is obtained from sources which we, and our suppliers believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. Neither our information providers nor we shall be liable for any errors or inaccuracies, regardless of cause, or the lack of timeliness of, or for any delay or interruption in, the transmission thereof to the user. With respect to information regarding financial performance, nothing on this website should be interpreted as a statement or implication that past results are an indication of future performance.