What has become clear following the destruction of government treasuries this past week, besides the fact that we are entering a new era of exponentially higher interest rates that pretty much nobody in the current generation of investors has experience dealing with, is that the equity markets have very little room for error moving forward.

When you have competing government backed assets that are getting close to handing you 4% without a shred of risk barring global thermonuclear war, then equities have to be on their best behavior.

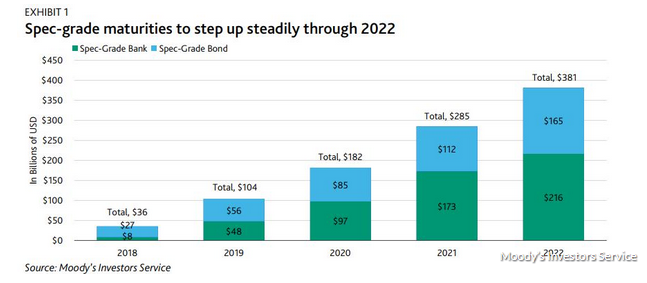

The biggest problem for companies on a more micro level is that there is debt that will have to be refinanced in the years ahead, with an abundance of debt coming due after 2020. What if the yield on the 10 year at that point is above 5%? What will refinancing debt with literally double the level of debt service do to corporate profits? Will growth in profits over the next 18 months be able to mitigate the increased debt servicing costs?

This type of maturity wall into a markedly higher interest rate environment very simply sets up a profit abyss for many companies moving forward. It is becoming more important, as portfolios are balanced and rebalanced in the months ahead, to be cognizant of companies that will be subject adverse conditions of suddenly taking on increased debt service costs at figures that have been completely outside of their ability to forecast.

To simplify this to the maximum degree possible, anything that derives income from yield will do well. Anything that derives income from borrowing will struggle.

Adjust accordingly.

_______________________________________________________________________________

From time to time, I email individual company research, commentary and excerpts from my monthly investor letter to those who are interested. If you would like to receive future emails, please write me at mail@T11Capital.com

Disclaimer

This website is for informational purposes only and does not constitute a complete description of our investment advisory services. No information contained on this website constitutes investment advice.

This website should not be considered a solicitation, offer or recommendation for the purchase or sale of any securities or other financial products and services discussed herein. Viewers of this website will not be considered clients of T11 Capital Management LLC just by virtue of access to this website.

T11 Capital Management LLC only conducts business in jurisdictions where licensed, registered, or where an applicable registration exemption or exclusion exists. Information contained herein is not intended for persons in any jurisdiction where such distribution or use would be contrary to the laws or regulations of that jurisdiction, or which would subject T11 Capital Management LLC to any unintended registration requirements. Visitors to this site should not construe any discussion or information contained herein as personalized advice from T11 Capital Management LLC. Visitors should discuss the personal applicability of the specific products, services, strategies, or issues posted herein with a professional advisor of his or her choosing.

Information throughout this site, whether stock quotes, charts, articles, or any other statement or statements regarding capital markets or other financial information, is obtained from sources which we, and our suppliers believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. Neither our information providers nor we shall be liable for any errors or inaccuracies, regardless of cause, or the lack of timeliness of, or for any delay or interruption in, the transmission thereof to the user. With respect to information regarding financial performance, nothing on this website should be interpreted as a statement or implication that past results are an indication of future performance.