What follows is a section from the “Thoughts & Analysis” portion of my monthly letter to investors at T11 Capital.

Confusion Is The Path of Lease Resistance

It remains an extremely simple exercise to look at the circumstances surrounding the current evolution of this bull market and determine that it cannot last. Not much has changed since the inception of this secular bull market in 2013. Doubting the ability of equities to ascend remains the path of least resistance.

While it is true that bull markets climb a wall of worry, that wall of worry is often times built on facts that markets do not immediately become concerned with, instead choosing to revel in glorious optimism without concern for what lies dormant in the background. In fact, one of the lessons of experience in finance is that markets very often take longer to react to important developments than one would suspect. The emotions of the day very often take precedent over relevant facts, whether micro or macro related, that have very real consequences for the economy, earnings etc.

The markets do a wonderful job of behaving in a nonchalant fashion as important changes occur that immediately concern market observers who then decide that given the markets predominance in one direction, their concern is unwarranted. The important fundamental shifts occurring in the background never go away, of course. They simply lie dormant awaiting the moment when the emotional tank of investors moves to empty.

This applies to individual stocks just as much as the broader markets. Individual stocks, especially in my favored category of sub-$500 million in market cap, can take months or years to awaken to fundamental developments that have been percolating in the background while the stock price languishes causing a majority of investors to think that their analysis was wrong, when in fact, their analysis was simply on delay. Companies can often times experience multiple years worth of gains in just a few months as they catch up to the fundamental realities that investors suddenly awaken to.

Much like a badly dubbed Chinese Kung-Fu movie where the words are heard before the mouths of the actors begin moving, there is an inherent delay in individual equities and the markets in realizing important fundamental developments. More often than not, the confusion that most investors experience is a result of this delay, giving rise to often used descriptive terms to describe the markets such as illogical, counter-intuitive and contrarian in nature. Markets may, in fact, be much more logical than we realize. However, they are also much less efficient in factoring in relevant developments than we realize, as well.

This lack of efficiency as it applies to the general market currently is being expressed as a market that is ignoring the fact that the impetus for the currently rally may not be as potent as originally expected. Bringing me to the next section of Thoughts & Analysis.

Legislative Morass

While the markets have experienced some downside volatility in response to the fact that both the White House and Congress are in a state of general disarray, the downside volatility has been reluctant to persist because animal spirits of the day still rule the markets.

This is perfectly normal behavior at this stage of the bull market. Important fundamental developments, such as the failure of repeal and replace of the ACA which has a direct impact on the probability of significant tax reform, are being rightfully seen as important enough by market participants to sell equities. However, there are enough participants who are underinvested that the downside is bought. There also seems to be an inordinately large contingent who continue to try to time the top of this secular bull market. For example, on the gap down day of Monday the 27th , the put/call ratio opened above 2.00, behavior typically reserved for prolonged declines. Not declines that have the S&P 500 just 1% off all-time highs.

The problems of government are coming against the backdrop of a Federal Reserve that is now in full scale rate increase mode. While normalizing the fed funds rate is justified at this stage of the economic cycle, there are certainly ramifications, especially if yields on treasuries continue to move up, making stocks more expensive. Downward cycles in the markets are often times preceded by rising yields that compete for investment dollars against stocks, until it finally gets to a point where the risk free rate of return becomes a no-brainer in the face of inflated equity values. While we are not at that point here and now, investors do for the first time in recent memory have a ticket to that ultimate destination.

Markets also seem to be awakening to the fact that a 15% corporate tax is a virtual impossibility given budget constraints, especially in the face of no budget savings coming from the repeal of Obamacare, which was key to the initiative. This leaves the 20% idea which hinges on the idea of the a border adjustment tax, a political nightmare for an already embattled Republican party that does not have the solidarity in place for such drastic reforms to the tax code. So 15 and 20 percent corporate tax rates are out the door.

As I said on Twitter the day after elections, the corporate tax rate will settle around 25-30 percent after all is said and done. It will be a token tax cut in the end. The possibility does also exist of no tax cut at all as the president's adversaries in Congress are literally everywhere. As his approval ratings drop so will the ability of those around him to cooperate for fear of losing their seats.

All of this points to an extremely difficult second half of 2017 as the market's mouth takes time to catch up to the words coming out. I continue to believe we have a few more months of upside left that can actually be dramatic in nature. However, beyond that point, the specter of rising rates, a dysfunctional government and premium stock prices does set the market up for a difficult period.

Our current portfolio is setup defensively as a majority of our assets are in two investments: A shell company that benefits from the lack of a cohesive government and cheaper overall valuations and an insurance company that is in an industry that is inherently defensive while having the added benefit of becoming more profitable with higher yields. Generally speaking, technology growth and financial names could be in precarious positions past June.

While the markets seemingly ignore the fundamental developments of the past few months, often times everyone decides to pay attention at once and it typically happens right at the time when a majority of buyers are invested and a majority of shorts have covered, leaving little in the way of bid support to stabilize equities.

Some Interesting Charts

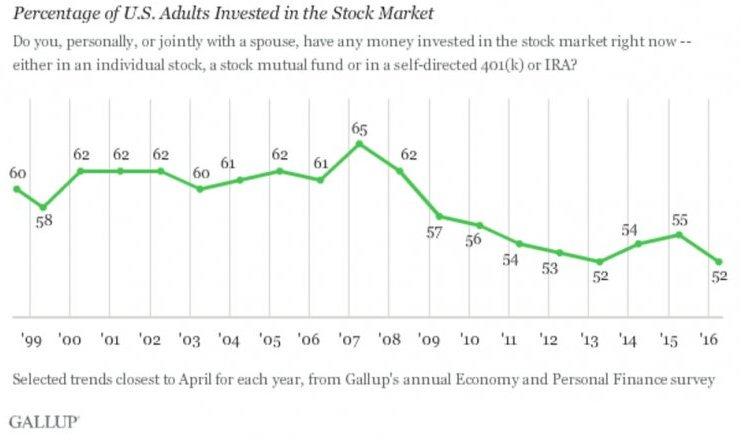

When you consider the persistence of this bull market to the upside, this is an astounding chart. There is deep skepticism in anything that hints of “establishment,” with the stock market being seen as one of the pillars. In the end, it will be mistake to underestimate the propensity for human greed, however, as markets have a tendency to force the hand of everyone before secular changes in trend.

We are experiencing a dramatic expansion in price earnings ratios at this stage of the bull market. Expansionary P/Es are part and parcel during mid to late stages of a secular bull market rally. As we are currently in what I believe to be the mid-stage of this secular bull market, P/Es have much further expansion ahead. Before the end of this secular bull, there may be a redefinition of what actually constitutes “expensive” in the stock market. Per the usual, those relying on unreliable fundamental tools that are subject to unpredictable expansionary periods determining the markets are expensive will suffer by either being out of equities early or short the market, in the most disastrous scenario. Surprisingly, there is already a substantial contingent of these wrongheaded investors. Expect their calls to grow exponentially louder in the years ahead, as the markets continue to defy their measures of valuation.

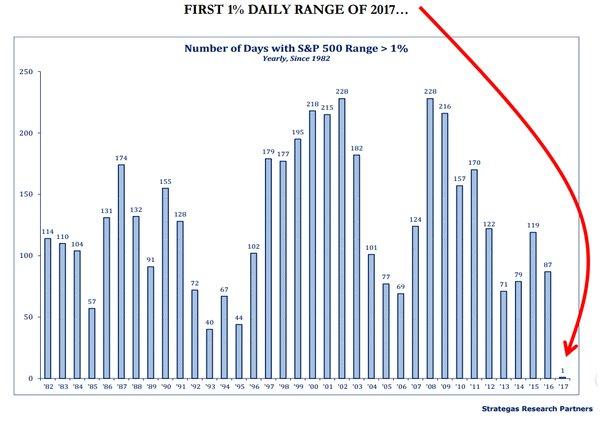

The quarter that just passed was the least volatile in roughly 50 years. Expansionary volatility in bull markets is typically a sign of an impending change in trend. The lack of volatility we are experiencing bodes well for further gains over the long-term. I would expect to see multiple years of expansionary volatility before a substantial market top is seen, similar to the late 90s.

Overall, as I have been emphasizing for some years now, the best strategy remains to remain invested in equities with a long-term perspective. Investors have an uncanny ability to get in their own way by overthinking situations that require little to no thought at all. The ability to simply sit still is increasingly becoming a rare form of behavior among all individuals, regardless of pedigree, occupation or class.

Regards,

Ali Meshkati

Disclaimer

This website is for informational purposes only and does not constitute a complete description of our investment advisory services. No information contained on this website constitutes investment advice.

This website should not be considered a solicitation, offer or recommendation for the purchase or sale of any securities or other financial products and services discussed herein. Viewers of this website will not be considered clients of T11 Capital Management LLC just by virtue of access to this website.

T11 Capital Management LLC only conducts business in jurisdictions where licensed, registered, or where an applicable registration exemption or exclusion exists. Information contained herein is not intended for persons in any jurisdiction where such distribution or use would be contrary to the laws or regulations of that jurisdiction, or which would subject T11 Capital Management LLC to any unintended registration requirements. Visitors to this site should not construe any discussion or information contained herein as personalized advice from T11 Capital Management LLC. Visitors should discuss the personal applicability of the specific products, services, strategies, or issues posted herein with a professional advisor of his or her choosing.

Information throughout this site, whether stock quotes, charts, articles, or any other statement or statements regarding capital markets or other financial information, is obtained from sources which we, and our suppliers believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. Neither our information providers nor we shall be liable for any errors or inaccuracies, regardless of cause, or the lack of timeliness of, or for any delay or interruption in, the transmission thereof to the user. With respect to information regarding financial performance, nothing on this website should be interpreted as a statement or implication that past results are an indication of future performance.