What follows is a section from the “Thoughts & Analysis” portion of my monthly letter to investors at T11 Capital.

The Haunted House of ZIRP and NIRP

Zero interest rate policy, more commonly referred to by the acronym ZIRP, has worked its way into the financial lexicon over the past year in a rather eloquent manner, followed closely by negative interest rate policy or NIRP. Financial pundits of all types have taken to the airwaves proclaiming ZIRP and NIRP as something that is an inevitable conclusion to the massive global monetary stimulus that continues to take place.

Denmark, Sweden, Switzerland and Japan are all wandering into the haunted house of ZIRP and NIRP currently, wondering what lies in its hollow corridors and narrow passages. There is no guidepost for ZIRP and NIRP, as it has never been attempted in such a globally coordinated fashion.

What lies at the essence of ZIRP and NIRP policy is a proclamation by global central bankers that cash is essentially worthless unless invested in a risk asset. This proclamation comes against a backdrop of investor skepticism of risk assets moving progressively higher on the curve based on the substance of the asset in question, with stocks being seen as the least substantive taking a backseat to tangible assets such as gold and real estate.

Most recently, even centers of reliable increases in real estate prices that have attracted global assets, such as New York and San Francisco, have seen a general softness in prices develop as the uncertainty of this experiment in global monetary policy has taken its toll.

What must be considered is that against a backdrop of enormous uncertainty created by a never before attempted policy of ZIRP and NIRP, will investor mentality begin converging along the lines of low or no returns available in all asset classes causing them to simply refuse to participate in all but cash for an indefinite period of time?

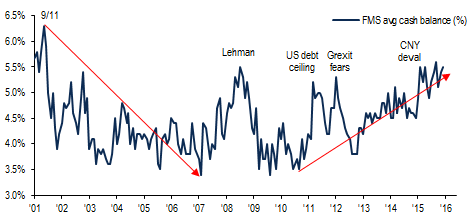

Already global cash levels are at 15 year highs according to some measures such as the Bank of America Merrill Lynch Global Fund Manager Survey: Global investors' cash levels are currently pegged at 5.6% of their total portfolio, which is the highest in the past 15 years as many have opted for capital protection amid a volatile global market.

This mentality towards capital preservation in the face of an attempt by global central banks to force investors out of cash tells us at a very basic level that investors see no returns as a better option than a negative return. We have to assume then that investor expectations for future returns are being tempered by the day.

I'm not going to pretend to know the outcome of the ZIRP and NIRP policy on investment returns for various asset classes moving forward. What I can say with some confidence is that investors initial knee jerk reaction of moving to cash with a zero effective yield is more than likely rooted in misinformation and emotion, which markets inherently enjoy taking advantage of to the detriment of those participating.

By no means should the influence of witnessing near zero returns for fixed income investments be underestimated as a negative deterrent to equities. This is the opposite of the intended effect, which is to push assets out of fixed income into risk assets. However, chronic pessimism with respect to global equities paired with further pessimism for the prospect of any returns whatsoever as dictated by little to no risk-free yield being available for capital has caused a cloud of insanity to take over the mind of investors.

Wall Street tends to counter insanity through either extreme acts of fear or perverse acts of greed. Meaning that Wall Street has the inherent ability to counter misallocations of capital, as is taking place currently with investors seeking zero yield through fixed income, through the manipulation of investor emotions.

It is unfortunate that although a majority of investors claim to be contrarians, very few will properly take advantage of this environment through the purchase AND investment in value stocks. Instead, what is likely to take place are short-term rentals of value stocks that are sold in short order, missing out on a majority of the adjustment upward that is likely to come.

I'll end this section with a chart clearly demonstrating the divergence taking place between value and growth stocks in the market much to the advantage of patient value investors, followed by a quote by Jesse Livermore:

It is no trick at all to be right on the market. You always find lots of early bulls in bull markets and early bears in bear markets. I’ve known many men who were right at exactly the right time, and began buying or selling stocks when prices were at the very level which should show the greatest profit. And their experience invariably matched mine that is, they made no real money out of it. Men who can both be right and sit tight are uncommon. I found it one of the hardest things to learn. But it is only after a stock operator has firmly grasped this that he can make big money. – Jesse Livermore

May Edition of “I'd Rather Eat Rocks Than Buy Stocks”

Equities continue to exhibit a repulsive quality that has made them the envy of maniacal despots, both dead and alive. The hate for stocks reached a fever pitch in May, despite the fact that the S&P 500 is a mere 1% away from all-time highs.

The proclamations of an imminent crash have become so widespread in the financial media that both individual investors and institutions have had no choice but to bend to this mentality in what is essentially a melding of the minds between punditry provided by media personalities and professional analysis provided by investment managers/analysts.

Below are examples from both far and wide that show stocks in 2016 are as loathed as anytime in recent memory, including the financial crisis:

Companies are too skeptical of public market demand to IPO

The average cash balance among institutional investors is at crisis levels in anticipation of the next crisis

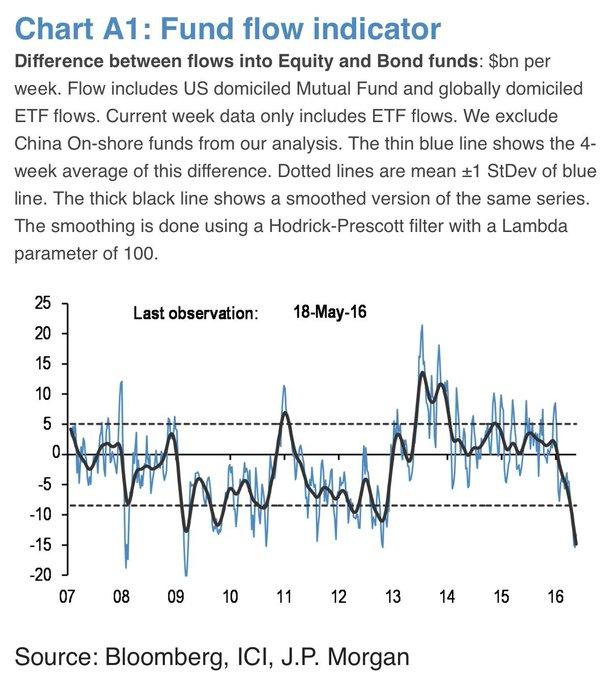

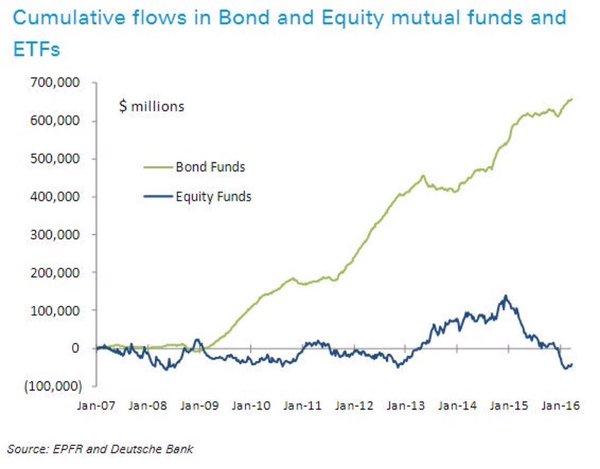

Money is flowing into bonds despite a near zero yield and avoiding equity funds entirely

According to a recent Gallup Poll, the level of investment in equities is at a 16 year low

A visualization of the positive flow into bond funds versus flow into equity funds

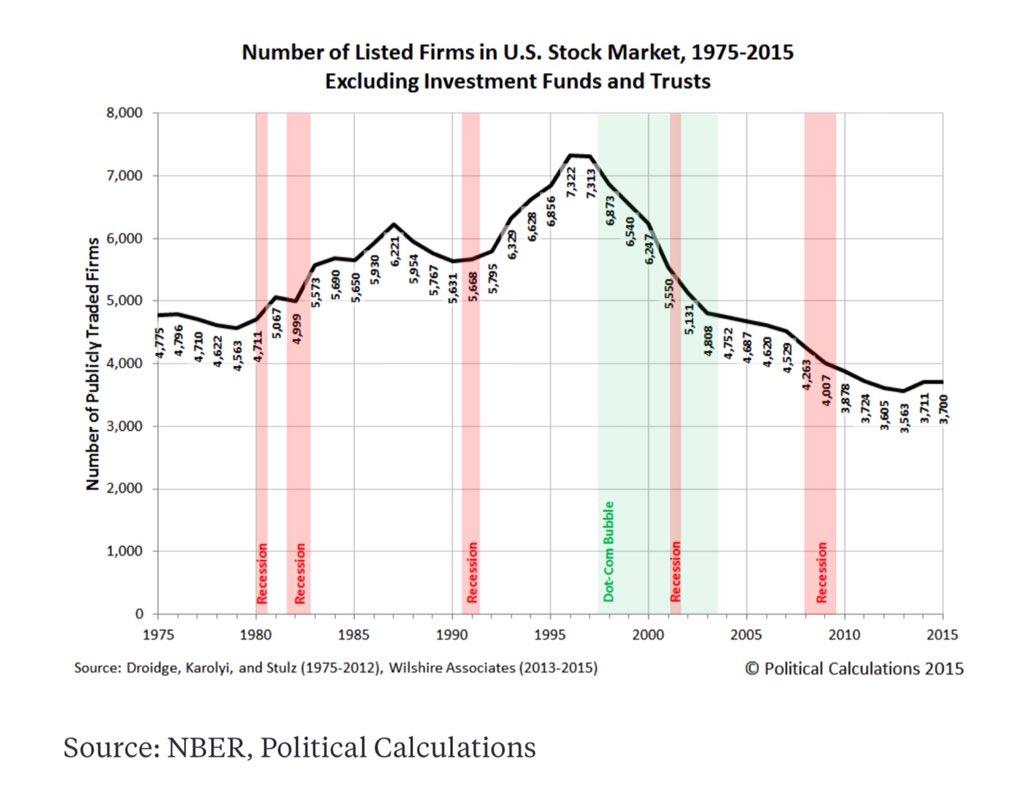

When demand returns to the equity markets there will be a supply shortage as listed firms have literally disappeared over the past two decades

American Association of Individual Investors survey shows the lowest reading of bulls in the history of the survey going back 30 years

According to ISI: 2015/16 net outflows from equity funds plus equity ETFs are already bigger than 2008/9 and it's only May.

"Equities continued to experience outflows and lost $3.32bn (-0.1%) last week, their 4th consecutive decline. Year-to-date, equity funds have lost $58.6bn (-0.6%), the largest ever dollar outflow in any 22 week period for the asset class"

Corresponding pessimism in the art market: After a blistering five-year boom of near limitless possibilities, it is suddenly getting tough in another asset class – one that mere commoner millionaires are not invited to play in: the high-dollar art market.

Auction house Sotheby’s reported on Monday that revenues in the first quarter plunged 32% from a year ago.

Regards,

Ali Meshkati